In this Issue:

- No overtime meal allowance, no overtime meal deduction

- Fringe benefits change for tax offsets from 1 July 2017

- FREE Tax Blaster Session

- Memorable Quotes…

- Increase to the SBE turnover threshold

- Reduction in the corporate tax rate

- Make Every Minute Count during the Workday

- Make Good Decisions with These Ingredients

- Costs of travelling in relation to the preparation of tax returns

- Laughter is the best medicine

- FBT: Cents per kilometre basis

- FREE Copy of Our Book

Only a few weeks until the end of the 2016-17 financial year, and there are a few things that you need to pay attention to this year, some of which we’ve covered in this newsletter. The Government has already enacted quite a few changes to taxation laws, and there are more to come starting 1 July, affecting businesses and their staff alike.

To help you get prepared for your tax return contact us for a 2017 Year-end Checklist for Business, so you can make sure to minimise your tax bill this year.

If you want more information on tax saving strategies, you can get a free download of our eBook “How to Slash Your Tax Legally”. Just visit the Resource Centre on our website to get instant access.

If you have any questions about the items published in this newsletter, please don’t hesitate to give us a call on 07 3399 8844… or stop by at our office for a coffee. We’re never too busy to sit down and talk to you.

Best regards from the Team

![]()

No overtime meal allowance, no overtime meal deduction

An employee construction project manager/supervisor was denied deductions for overtime meal expenses, as he was not paid an overtime meal allowance under an industrial agreement (award).

The taxpayer often worked at nights and on weekends during the relevant income years, and so additional amounts were negotiated and ‘rolled into’ his salary to cover the fact that he was expected to work additional hours, and also to cover any out-of-pocket expenses associated with such overtime.

However, the taxpayer’s salary was not paid under an award, which was simply used as a starting point in annual remuneration negotiations (and he was paid the same amount each week, regardless of hours worked or expenses incurred).

Therefore, the AAT agreed with the ATO, finding that the taxpayer had received no overtime meal allowance under the relevant industrial award.

As no deduction is claimable under the income tax law for overtime meal expenses unless an appropriate award overtime meal allowance is paid, the Tribunal swiftly dismissed the taxpayer’s appeal, and also affirmed the 25% administrative penalty.

Fringe benefits change for tax offsets from 1 July 2017

The ATO has issued a reminder that the government has changed the way fringe benefits will be treated for the calculation of several tax offsets from 1 July 2017.

The meaning of ‘adjusted fringe benefits total’ (which is used to calculate a taxpayer’s entitlement for the low income superannuation tax offset, the seniors and pensioners tax offset, the net medical expenses tax offset and the dependent tax offset) has been modified so that the gross, rather than the adjusted net value, of reportable fringe benefits is used.

Fringe benefits received by individuals working for registered public benevolent institutions, registered health promotion charities, some hospitals and public ambulance services will not be affected by this change.

This aligns the treatment for tax offsets to the treatment for the income tests for family assistance and youth payments.

FREE Tax Blaster Session

There are a number of ways that individuals and small business operators can legally slash their tax. We find that many of our clients only begin to realise after a chat with one of our professional tax agents how much tax they could have saved if they had taken action earlier.

Don’t delay it any longer and book in for your FREE 20-minute Tax Blaster session. We’ve got limited spaces available for people who want to increase their earnings, save on taxes and put more money into their retirement fund.

Find out NOW how you could be making more money for your retirement and facing less financial stress now and in future.

Call our Team on 07 3399 8844 to book your FREE meeting NOW.

Memorable Quotes…

“Education is the most powerful weapon which you can use to change the world.”

Increase to the SBE turnover threshold

As was previously announced, the Small Business Entity (‘SBE’) definition has changed with respect to the turnover eligibility requirement.

The aggregated turnover threshold has increased from $2 million to $10 million with effect from 1 July 2016 (i.e., the current, 2017, income year).

Note that, whilst the increase in this threshold will expand access to most SBE concessions (e.g., simplified depreciation), this change will not apply with respect to:

- the Small Business Income Tax Offset (a special $5 million threshold will apply when determining eligibility for this tax offset); and

- the Small Business CGT concessions (the aggregated turnover threshold to access these concessions will remain at $2 million, although taxpayers may still seek to satisfy the $6 million maximum net assets test as an alternative method of obtaining access to these concessions).

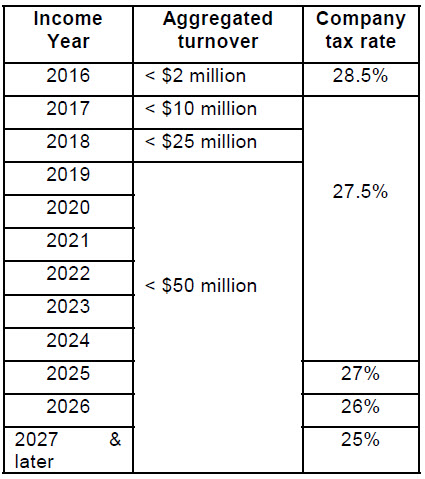

Reduction in the corporate tax rate

The most significant difference between the Government’s original proposals and what was finally passed by Parliament was in relation to the reduction in the corporate tax rate.

Although the corporate tax rate will still decrease to 25% (by the 2027 income year, as originally proposed), access to the reduced corporate tax rate will be restricted to corporate entities that carry on business with an aggregated turnover of less than $50 million (from the 2019 income year).

The following table provides a summary of how the progressive reduction in the corporate tax rate will apply.

Editor: As noted above, corporate entities with at least $50 million aggregated turnover or, more importantly, companies that do not carry on business (e.g., passive investment companies and ‘bucket companies’) will continue to have a corporate tax rate of 30%.

Make Every Minute Count during the Workday

Time is your most valuable asset at work. If you struggle to get everything done on time and accurately, consider this advice for managing your day more efficiently:

Question everything. Look at each task and ask, “Is this the best use of my time right now?” Delay or eliminate anything that’s unrelated to your most important responsibilities.

Eliminate distractions. If you have an office with a door, close it to prevent interruptions. If you’re in a cubicle, consider posting a “Do not disturb” sign when you need to concentrate or finding an empty conference room where you can work in peace.

Cut the tech cord. Don’t be a slave to technology. You may have to turn off your email alerts and silence your phone in order to get your work done. Check emails and voicemail on a regular basis, but not every five minutes.

Write tasks down. Instead of trying to juggle every task that comes up in your head, make a habit of writing things down as they’re presented to you. This helps you keep a clear mind, so you can concentrate on the immediate task.

Keep a schedule. Don’t just make a to-do list. Schedule each item on it, along with an estimate of how long each task will take. This helps you budget your time effectively throughout the day.

Make Good Decisions with These Ingredients

Succeeding on the job depends on making good decisions about projects, tasks, and solutions. Pay attention to these essential components:

Analysis. Gather only the facts you need, not every piece of data available.

Thoughtfulness. Take other people’s reactions and needs into account. You might not make everyone happy, but you want people to know you didn’t ignore their feelings.

Quickness. Don’t waste time. Take action once you’re confident you’ve acquired the information you need.

Commitment. Stick to your decision once you’ve made it. Change it only if the situation shifts.

Costs of travelling in relation to the preparation of tax returns

The ATO has released a Taxation Determination confirming that the costs of travelling to have a tax return prepared by a “recognised tax adviser” are deductible.

In particular, a taxpayer can claim a deduction for the cost of managing their tax affairs.

However, apportionment may be required to the extent that the travel relates to another non-incidental purpose.

Example – Full travel expenses deductible

Maisie and John, who are partners in a sheep station business located near Broken Hill, travel to Adelaide for the sole purpose of meeting with their tax agent to finalise the preparation of their partnership tax return.

They stay overnight at a hotel, meet with their tax agent the next day and fly back to Broken Hill that night.

The full cost of the trip, including taxi fares, meals and accommodation, is deductible.

Example – Apportionment required

Julian is a sole trader who carries on an art gallery business in Oatlands.

He travels to Hobart for two days to attend a friend’s birthday party and to meet his tax agent to prepare his tax return, staying one night at a hotel.

Because the travel was undertaken equally for the preparation of his tax return and a private purpose, Julian must reasonably apportion these costs.

In the circumstances, it is reasonable that half of the total costs of travelling to Hobart, accommodation, meals, and any other incidental costs are deductible.

Editor: Although the ATO’s Determination directly considers the treatment of travel costs associated with the preparation of an income tax return, the analysis should also apply where a taxpayer is travelling to see their tax agent in relation to the preparation of a BAS, or another tax related matter.

Laughter is the best medicine

Looking for a Job? Here’s What Not to Do

Looking for a Job? Here’s What Not to Do

Here are some things actual applicants for jobs have reportedly said or done during interviews:

“Stated that, if he were hired, he would demonstrate his loyalty by having the corporate logo tattooed on his forearm.”

“Interrupted to phone his therapist for advice on answering specific interview questions.”

“When I asked him about his hobbies, he stood up and started tap dancing around my office.”

“Said he wasn’t interested because the position paid too much.”

“A balding candidate abruptly excused himself. Returned to the office a few minutes later, wearing a hairpiece.”

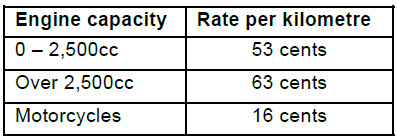

FBT: Cents per kilometre basis

The rates to be applied where the cents per kilometre basis is used for the 2017/18 FBT year in respect of the private use of a vehicle (other than a car) are:

Editor: The ATO also determined that the small business record keeping exemption threshold for the 2017/18 FBT year is $8,393.

FREE Copy of Our Book

We hope that you’ve enjoyed this edition of the Straight Numbers & Tax Talk.

As a Thank You to our readers we’ll give away a FREE copy of our highly sought-after book titled ‘Straight Money Talk – A Straightforward Plan for Financial Independence” (worth $17.95), PLUS the accompanying workbook “5 Steps to Financial Independence”.

In this book, Robert Bauman lays out 10 steps anybody can follow to become truly wealthy, and reveals ‘money myths’ and ‘inside secrets’.

Just contact us on 07 3399 8844 to claim your gift and we will send it out to you.

About Straight Money Talk—A Straightforward Plan for Financial Independence

WHAT PEOPLE ARE SAYING ABOUT THIS BOOK:

WHAT PEOPLE ARE SAYING ABOUT THIS BOOK:

“I’ve read many financial books and found this one to be up there with the best. It can really kick-start your journey to get your financial situation into great shape.”

– Dr. Joe Vitale, author “Attract Money Now” www.attractmoneynow.com

“Robert has done a fantastic job on this book. My views on how to handle money and how to educate my kids to learn the value of savings have totally changed now. This is an excellent book to guide you to creating great financial wealth in your life!”

– Keith Abraham CSP – Professional Speaker and Best Selling Author

Please Note: Many of the comments in this publication are general in nature and anyone intending to apply the information to practical circumstances should seek professional advice to independently verify their interpretation and the information’s applicability to their particular circumstances.